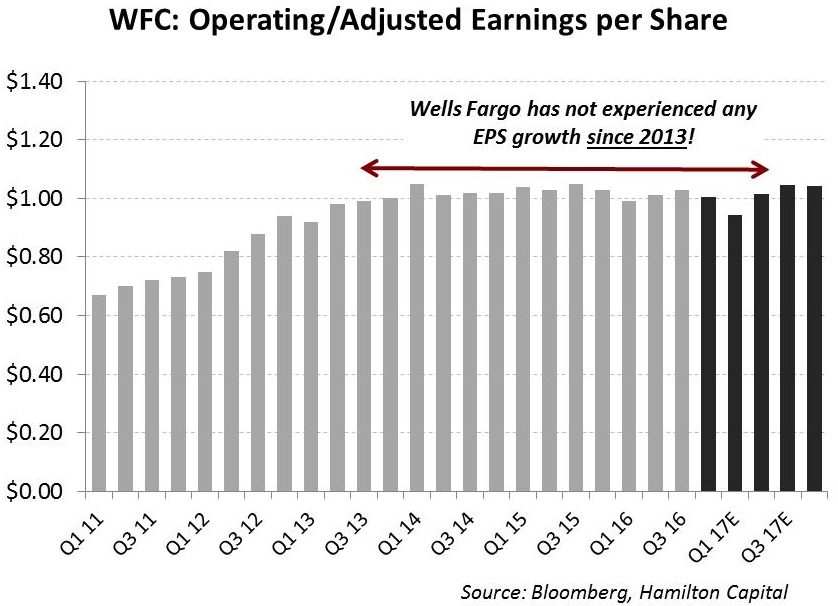

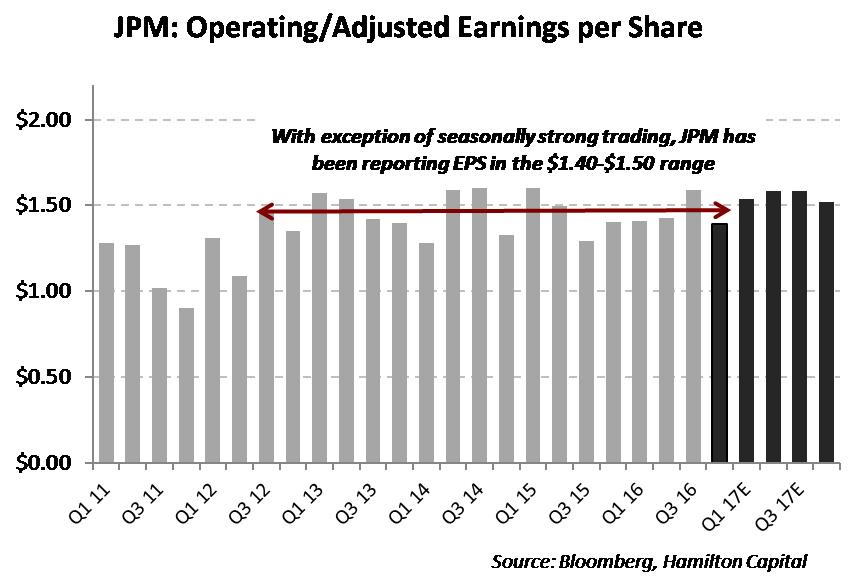

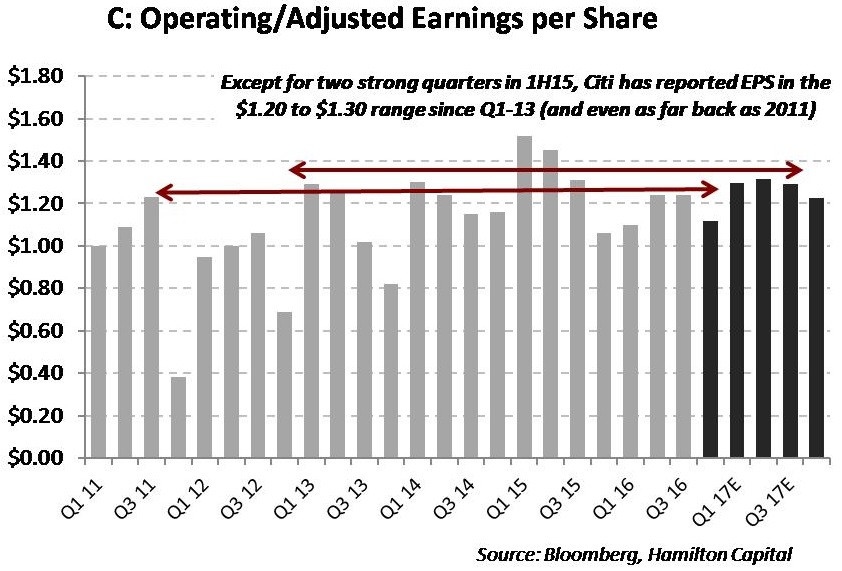

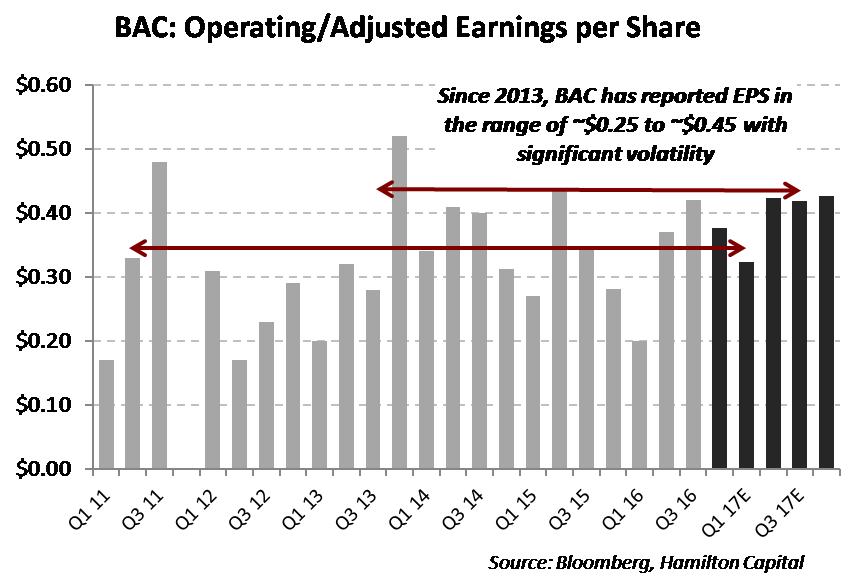

As we have indicated in prior commentary, we have zero exposure to the U.S. mega-cap banks, primarily because of their very low EPS growth, mid-single digit ROEs (in the case of C and BAC), and very high regulatory risk (see “Five Reasons We Don’t Own C, JPM and BAC”, June 14th). We favour a portfolio of U.S. banks derived from the nearly 200 publicly traded U.S. mid-cap banks given they have greater and more consistent EPS growth, are more rate sensitive, have lower regulatory risk, and are merging.

To illustrate just how difficult it has been for U.S. mega-cap banks to generate EPS growth in this challenging operating environment, the charts below highlight that Citigroup (C), Bank of America (BAC), JPMorgan (JPM) and Wells Fargo (WFC) are all entering their fourth year of very low-to-zero EPS growth.